CLIENT UPDATE - JAN 2018 Part 1 "Overall, we expect that the economy will continue to expand at a moderate pace over the next few years." -- Fed Chair Janet Yellen "We don't need the money." - Michael Bloomberg - referring to the tax reform legislation

The Return of Irrational Exuberance?

Perched atop the beginnings of a new year, even as stocks reach new historic highs seemingly daily, investors are struggling to make sense of a new world order. From anxiety to anxious euphoria, nightmares of global political disruption, threat of nuclear war with a Third World nation, and nature run amok on one hand, an economy gliding hrelike Fred Astaire and Ginger Rogers on the other. While investors look with some satisfaction - and disbelief -- at their increasing account values, many do so with a combination of anxiety and guilt.

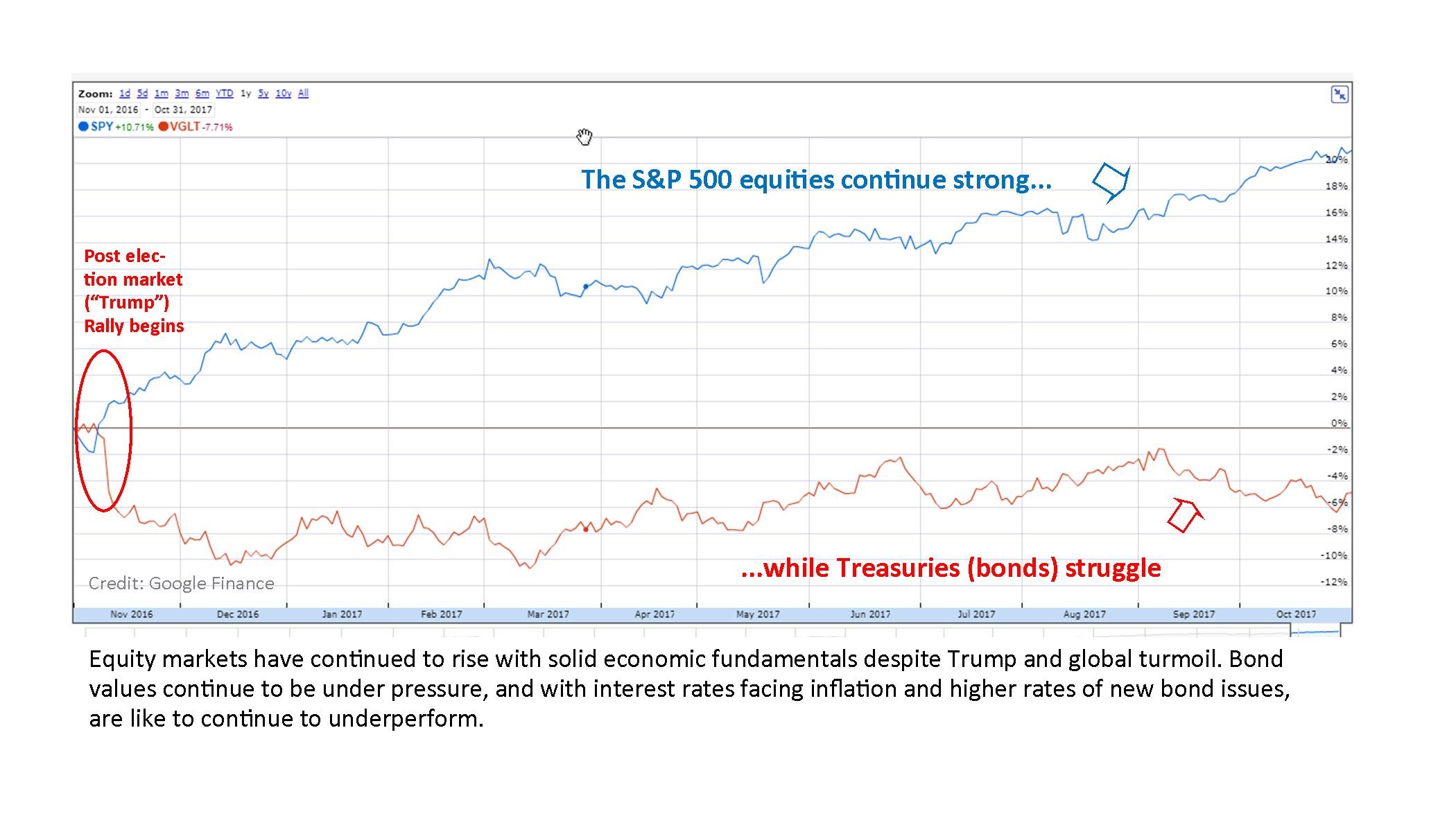

Despite the extreme run-up in equity prices - over 21% in 2017 for the S&P 500 -nothing certainly when compared to Bitcoin's 1,400% shot! -- volatility levels - fear -- remain extremely low, and concern is growing that complacency now could lead to a harder fall when things do in fact turn for the worse. And the biggest concern could be the bond asset class- which is struggling to stay above inflation and still at very high prices.

Looking forward into 2018, despite the strong economy, caution lights begin to flash: the uncertainty of the new Federal Reserve, the impacts of the recent tax legislation, and equity and bond markets that may be moving into unsustainably high levels . The winds of the feared "I-word", inflation, may be finally blowing in. If the economy becomes increasingly ragged late in 2018, will the stock market be able to maintain its upward climb from its already high prices? And with everything seeming so cozy now, what will happen when an unexpected shock hits the system - will the memories of the Great Recession come storming back from the painful past?

Our take is that this is a near "just right" Goldilocks economy - an economy coming out of a long, slow recovery which, in fits and starts, is finally humming along without any major laggards. It has been a long recovery historically, but still seems sound. Despite the child-President's insistence, this is an economy borne of a sound global economic system combined with thoughtful and meticulous central bank management post Great Recession.

Our biggest concern, aside from major geopolitical crisis, is overheating, and over the last few months, we are concerned that the combination of a sharp upward rise in market prices combined with the supercharging of the economy that the recently passed tax legislation stands to goose, that fear is growing. We're still pretty optimistic things can run further, but the risks are growing, and the tax legislation, if successful as an additional economic boost, could have highly negative consequences. We expect volatility to begin to pick up -- and it would be healthy for it to do so.

"Bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria." Sir John Templeton

Just when things were going good. When the financial markets start making main stream news headlines I get concerned. Over the last two weeks, in random conversations, non-financial conversations with normal folks talking about music, the weather, politics, I've heard more mention about Bitcoin, the "Trump Rally", Netflix, and stock prices than I have in years. And on the cover of daily publications on newsstands, the evening news, everywhere it seems the same refrain. It brings back recollections of two financial traumas I - and most investors - could happily have lived without: the Dot-Com crash of the late '90s and early 2000, and the Great Recession. I think asset bubbles, crashes, and the losers in musical chairs. Is this one of those times?, I find myself asking.

Wind back to the good ol' days of 1996. Those hard charging, optimistic Bill Clinton years when tech stocks began to dominate the conversation. Also the year that Alan Greenspan, quoting economist Robert Shiller, mentioned the term "irrational exuberance" in a speech. Back then, just 3 years before the major financial collapse in mid-2000, the S&P 500 had a reasonable price-to-earnings ratio of just over 18 times. Two years later, 1998, it was where we are today, nearly 25 times earnings. The fall was hard, indeed: the S&P 500 took nearly a 48% hit to prices, and the NASDAQ where some of those Dot.Coms resided, dropped a whopping 75%. But the crash wasn't until 4 years after 1998, and two years after those markets hit their highs in 2000!

So yes, there appears to be some historical precedent for a concern about a stock market drop where valuations are getting high. The key and interesting fact here is that we just don't know when. And guessing is a fool's errand.

The economy is incredibly sound - which we'll get to shortly. Were we able to strip away the recent tax legislation and the euphoria that seems to be pervading Wall Street with each new market high, we might be unconditionally optimistic about 2018 and years after. Had Congress and the Trump presidency not squandered a massive tax cut by making a donation to corporations and the wealthy investor class in the guise of stimulating growth, and instead chose to wisely invest in infrastructure and education we'd be far more sanguine about economic prospects in the future, instead of harboring an increasing concern about a significant pickup in inflation over the next year and a more challenging 2019.

"It's the economy stupid". Democratic strategist James Carville and Bill Clinton's lead campaign strategist's simplistic, yet sharp words hold as true today for the markets as they were intended to apply to politics. For the most part, the equity market will perform well when the economic prospects are good. Pretty much everything that has been working in the economy over the last few years continues to, and certain important elements are kicking in - as predicted - to speed things along. Most every economic sector is now alive,(e.g. wages, manufacturing) if not thriving, business spending and sentiment are improving, and exports are rising. Residential construction, one of the recent laggards of late, is being buoyed significantly and in short order as rebuilding begins in the aftermath of nature's fiery fury in California.

While December's addition of 148,000 workers to the workforce is a decided drop from some of the earlier numbers of the year, it is part of a long seven year trend of a steadily increasing workforce. The current unemployment rate, at 4.1% remains the lowest in recent history, and the number could drop further in 2018, suggesting an economy nearing full employment despite the disruption from the hurricanes in the Third Quarter of 2017. What's more, the benefits are broad based across different economic levels and race/cultural backgrounds.

Indeed, a skilled labor shortage has been an increasingly loud concern voiced by the corporate sector recently - which could become a structural issue going forward.

Consumer confidence, predictably, is sky high, at its highest level since 2000, even while the President's approval ratings are plunging toward Nixonian depths (so much for the "Trump trade") - something very atypical.

Most all of the other key economic factors are in good repair in the US. Consumer spending generated a strong holiday retail season, business spending is up, and manufacturing is strong, with manufacturing exports benefitting from a weaker dollar (allowing US goods to be cheaper to other nations). Energy prices have recovered - oil prices, have doubled to around $60 from their $30 per barrel lows back in Jan 2016 to a level that is now profitable for energy producers, but not so high as to choke off an economic recovery. Home prices are up. The one downside is that household savings is dropping, and getting near very low levels, a sign that some overheating may be taking place.

"Synchronized global expansion" is the touch phrase these days in the economic universe, as the economies globally are showing strength as well. Emerging markets exploded last year, China and Asia generally saw significant growth in 2017, and the developed economies in Europe are just now looking at pulling back from their stimulative monetary policies, running about a year behind us in their business cycle. Developed nations even outperformed the US Equity Markets last year, up 25%. Our treatment of Nature aside, we have truly recovered from the Great Recession of 2007 as a Planet.I personally cannot recall a global market when so many equity markets were moving upward so effectively, this due to the recovered economies here and abroad. So far so good.

Corporate Earnings. As we've probably mentioned in every newsletter we've ever written, ever, stock prices are about expected corporate earnings over the long term. The good news continues here, which is underpinning the new market highs among the large cap stocks (big corporate earners). Continuing a strong positive trend, corporate earnings are showing solid growth, with future earnings growth continuing at a healthy 10% plus annual rate. In the most recent earnings reporting period, nearly 3/4ths of companies beat their estimates, an above average number, and the good news covered the gamut of sectors (except insurance companies having to cover the costs of one disaster after another).

Some might argue that the current S&P 500 P/E (price to earnings) ratios are above average and that stock prices are too high. They are. Earnings growth from the S&P averaged just over 10.5% -- a very good number, but not something that is likely to continue indefinitely. The reality is that while the S&P was trading pretty much in its average range since 2000 - even removing the extremes from 2000 and 2008 - it's starting to get to levels higher than we'd like. Not crazy high, like in 2009 or the early 2000's, but at just over 25 times (trailing) earnings, a drop in price has to be expected. So if nothing else, investors should not be surprised by some significant market drops over the next year, even if short lived (and something we might see as healthy).

There is no mistaking the threats, however. The biggest issue clearly remains the bluster and tempestuousness of the child-President, although there has been some tempering of that behavior these last few months by those tending his cell. North Korea and other global entanglements remain concerns. Congressional dysfunction, which has put the kibosh on budget busting healthcare reform, has frankly been an economic stabilizer thus far, but cannot be counted on to continue. And the tax reform package - nay, tax cut to the investor class - could be, if successful, a key igniter of too-rapid growth or run-up in stock prices resulting in a new Federal Reserve forced to take heavy action to ward off the inflation demons.

The other potentially negative impacts on an otherwise smoothly running economy could revolve around a Trump-instigated trade war with a major economy, with China being front and center in the administration's sights. Economists across the board excoriated the administration for pulling out of the Trans Pacific Partnership - an agreement that, despite its flaws, could have helped contain Chinese economic power throughout Southeast Asia and strengthened the US. While there are legitimate issues with certain trade practices with China, the saber rattling in October and November are as likely to have a strong negative consequence as anything else. China's retaliation against the US would not only imperil our economic recovery, but could further destabilize the situation with North Korea.

But China is not standing alone in Trump's sights: even allies and major trading partners Canada and Mexico are looking at economic uncertainties in their economic relationships with the US. These are deeply troubling.

Inflation & the Fed. With the sage, grandmotherly Janet Yellen walking through the exit doors to be replaced by new Federal Reserve Chair Jim Powell, many are concerned about changes in the Fed's approach. Indeed, it seemed that the majority of Fed watchers and business leaders were strongly supportive of Yellen's reappointment, but with the new President, that was simply not to be. In choosing Powell, who has been a member of the Fed board since 2011, Trump chose a non-academic, highly successful attorney and hedge fund leader who is seen as someone who will likely follow in Yellen's "dovish" footsteps for the time being at least - e.g. inclined to support the Fed's taking an accommodative stance on the economy, as compared to the inflation "hawks" who will be seeking to slow the economy at the first whiff of inflation.

The bigger issue with the Fed is not Powell, but the potential make-up of the new Fed board members, as the appointments move away from academic excellence back to business interests, with a very anti-inflation philosophy - "inflation hawks". With the recent nomination of the uber-Hawkish Marvin Goodfriend, and Trump's desire to utilize his two remaining nominations to placate the Republican orthodoxy, the danger is a Federal Reserve hell-bent on stifling inflation at all costs. Three rate hikes for 2018 are reasonably in the offing as things return to normal. But who knows what an immoderate Fed is likely to have in store and its impact on an aging bull market? Moreover, the Fed may not have much choice if inflation fires up.

Without any help from the recent tax cut however, inflation is a growing concern. Although still very low historically, just around 2%, inflation iss likely to start moving up as wages and consumer spending grow, and that in turn will push up interest rates. Inflation has two impacts - first, it reduces that value of current goods and services, as $1 purchases less as prices go up. Second, and less directly inflation ultimately pushes up interest rates, in part because central bankers attempt to manage inflation by making it more expensive to borrow - a conversation for another time.

But this gets back to our concern - that inflation, leading to higher interest rates, means a slowing economy. And if the economy is being supercharged by tax legislation intended to stimulate the economy, for example, it could lead, ironically, to monetary policy to aggressively throttle the economy down, resulting in a market decline.

Taking It All In. From an investment portfolio perspective, here's where we find ourselves. With the economy expected to amble on for the next several months, we see potential for the markets to continue to rise, and for some of the "value" equities to start to outperform. We continue to see considerable stress on bonds, however, which are very richly priced, and dealing with an increasing interest rate environment. But we do see commodities and some other asset classes continuing to do well in this early inflation phase.

In the near and middle term, we remain generally optimistic about the economy and equity markets (with some significant hiccups). Bonds will, however, be under siege. We are really focused on inflation and further government actions (negated trade deals or worse), and insights into the Federal Reserve Bank that could provide greater clarity. In the meantime, keep your eyes open for the "mainstreaming of finance" - if you find yourself engaged in conversations about finance, or Bitcoin, perhaps you'll see the yellow alerts as well.

Ron Stein, CFP

Good Harvest Financial Group

631.423.6501

rstein@goodharv.com