A Virus Spreads to Wall Street

Dear Client & Investor:

ISIS. Hong Kong demonstrations. Ukraine. And now Ebola. The markets tend to be rational .until theyre not. As the equity markets near correction territory some down nearly 10% since their September highs and conceded any gains for the year, we need to ask why. Is this something which reflects the prospects of future earnings and economic growth, or is it tied to the spate of depressing news across a variety of fronts thats dominated the headlines? If the market volatility represents legitimate concerns about the economic landscape then it would be wise to factor this into portfolio decisions. On the other hand, if this is predominantly an emotional response to the uncertainty of geopolitical events that have little bearing on the economic fundamentals, combined with some natural profit taking after a long upward run in equity prices, then this glitch should not only be temporary, but perhaps a buying opportunity. Frankly, we are inclined to believe in the latter.

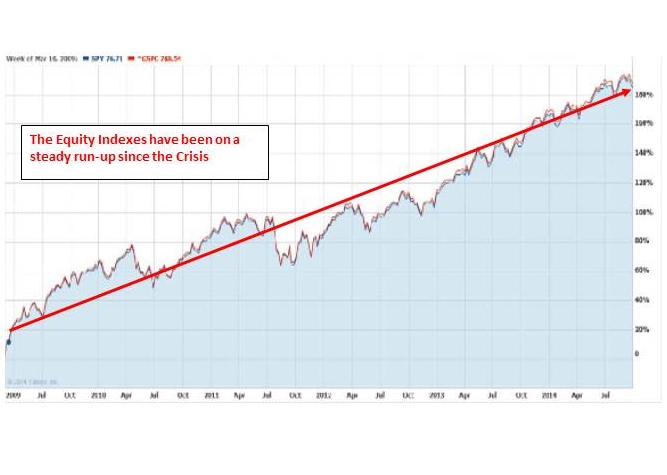

Let's consider the evidence. The equity markets have more or less moved in lockstep with the slow but fairly consistent economic growth since the financial crisis ended in early 2009. There have been several pullbacks during this six year period, some significant, but they have been temporary, and equity markets made new highs this year. Despite decent earnings news and solid fundamentals just two months ago the Fed was making clear its intent to begin raising interest rates in 2015 given the improved economy stocks were getting a bit pricey after their long run-up, although not overly so, trading at the higher end of their historical averages. Almost all the key indicators reflected continued, albeit slow economic growth: new jobs were being added monthly in substantial numbers, few people were on the unemployment rolls and the unemployment rate continues to drop. Productivity has been good, confidence rising in the business sector, interest rates for borrowing continued to be unusually low. Manufacturing output was decent across the board, housing and construction spending have improved considerably nationally, and personal income and consumption continues to improve.

And all of this good news while inflation has been unusually low, both on the consumer and producer side. This has been helped by the drop in energy and commodity prices, which has not only given consumers more disposable money in their pocket, but allowed producers to produce at lower costs. Consider the extraordinary drop in oil prices recently: from over $100 per barrel (already 1/3rd lower than prices during the crisis), to less than $80, resulting in lower gas prices, and lower heating and energy costs for consumers.

S&P 500 Since the Great Financial Crisis

Yahoo Finance

The weaker economic news really has been about Europe, where growth remains illusory. The inability of European Central Bank President Mario Draghi to institute the kinds of growth stimulating measures taken by the US Federal Reserve several years ago has left Europe in a Twilight Zone of sorts, as even powerhouse Germany is looking at a recession. Lacking appropriate central bank intervention, many economists are forecasting a low or negative growth environment for Europe in general for the foreseeable future, which casts a pall over US corporations who rely on heavy sales in Europe. Still, Europe represents but a small part of the overall US economic engine, so its impact should not be overly significant for the broader markets, although it could impact some of the larger multinational names. The markets, however, have largely factored a weak Europe into their stock prices.

Still, the Federal Reserve, ever cautious under both past president Ben Bernanke and now Janet Yellen, clearly recognizes the US economys strength, evidenced by both Yellens public comments, the Fed minutes, and the winding down of its stimulus measures: Quantitative Easing (QE2) is ending this month, and the Federal Funds rate, now near 0% is slated to finally begin increasing in 2015. Moreover, Yellen remains committed to continued US growth and has repeatedly indicated that the Fed is prepared to reintroduce measures that will maximize prospects of achieving its dual mandate -- managing inflation and maximizing employment and will take the necessary actions to keep the economy growing. What this tells us is that should the Fed see a hiccup in the US economy, theyre prepared to step in.

Still on solid ground. So despite Europes economic malaise, the US economy continues on reasonably solid footing, and remains the best economy globally and the most viable market environment. And the evidence overwhelmingly supports that scenario continuing for the foreseeable future. In reality, very little has changed meaningfully over the last 6 months. Very little.

The bad news? Sure, retail sales slipped a bit. New job creation is slower than desirable, and wages have been horribly stagnant for years. The average consumer doesnt feel much better off and is still sensitive to a repeat of the near financial collapse of 2008. And neither Germany nor the European Central Bank seem ready at the moment to take on the politically difficult challenge of stimulating the European economy and further incentivizing the fiscally questionable behaviors of Greece, Portugal, France and other nations who have run up negative balance sheets. We believe that at some point that will have to change. With its own economy in the doldrums, Germany can no longer afford the luxury of continuing its overly self-righteous approach to the economies of southern Europe.

Back to where we are now. Weve spoken many times about the impacts of uncertainty on economic markets, how fear is a huge driver of short term behavior among the ostensibly intelligent investing public, and how fear will trump greed almost every time. The fear and uncertainty are less about the economic fundamentals but about the world outside: ISIS, Ukraine, Hong Kong demonstrations, fed by the news headlines and talking heads throughout the media intent on locking in everyones attention.

As we saw during the SARS crisis and the Asian equity markets in 2002-2009, prospects of a cinema-like biological Armageddon quickly dominate the imagination causing a tremendous fear response, and were seeing the same thing with the Ebola-based market spasms. Every day, with our collective attention riveted on possible new victims and the growing fear of a terrible-case health crisis evolving here, that fear is translated to investors, and the market sell offs and volatility. This leads to a spiraling or domino effect, as fear-driven sales lead to tremendous declines, which only punctuates the fear laden atmosphere. Investors have fled stocks for bonds, driving stock prices down, bond prices up. Heavily leveraged hedge fund managers, expecting interest rates to rise with recent Fed Reserve pronouncements, and oil and stock prices to continue to gain, have been forced to sell shares of their large cap stocks by the millions of shares, further driving down prices.

So what to do? Begin by asking the simple questions: in an economy that continues to grow, is a company worth 10% less or more today than a month ago? Is a government or high quality corporate bond currently providing near historically low interest rates likely to be valued the same several years from now when we return to normal, and will interest rates be much lower in the future? Do you believe the Ebola issue were seeing in the headlines today will still be the dominant news item in six months, or two years down the road, and will the economy grind to a halt because of it?

We believe the answer is no to all these questions. We believe that somehow the health care infrastructure in the US will manage the Ebola virus. We believe the economy will continue to grow slowly going forward. We believe that the markets will either be pleased about the prospects of a Republican led Senate or satisfied that the status quo will be in place if the Democrats hold the Senate. We believe that the US economy will remain the economy of choice for the foreseeable future. We also believe that stocks today are becoming attractively priced, and particularly given the very low interest rates on bonds, a viable option for most investors. We may suffer several months of uncertainty, particularly as the geopolitical concerns in the Mideast, Ukraine, and Hong Kong remain in the headlines, but that these issues will find their way to the middle pages, invariably replaced by other concerns.

The only scenario we can envision that might lead to another major financial crisis is not that Ebola will truly spread contagion, but that the fears in the markets today result in such strong selling pressure that banks and credit markets, in an environment of tremendous uncertainty, become fearful of lending and credit dries up, creating a scenario similar to what took place in 2008. This is most unlikely, however, and post-2008 the systems are in now place to help mitigate against those risks. We just dont see it happening.

Stay the course. Our approach right now is to first be vigilant regarding the prospects of the above or some other basis for a prolonged downtown, but also to consider taking advantage of the market opportunities, selectively purchasing where appropriate, and trimming where we see elevated risks. With that said, we can sum up our position for longer term investors in a nutshell: as we feel that the probabilities still remain that these gyrations are likely to be temporary, we continue to recommend sticking largely to the overall target asset allocations. Shorter term investors, or those who cant stomach the volatility should begin to move to the sidelines over time. Keep in mind, however, that even with the worst financial crisis experienced in our lifetimes between 2007-2009, over time the equity markets recovered fully. They always do.

We wish everyone well and a beautiful and colorful Fall. Of course, peace to all. And please feel free to call with any questions.

Ron Stein, CFP

Good Harvest Financial Group

631.423.6501

rstein@goodharv.com